On talk vs action on digital healthcare

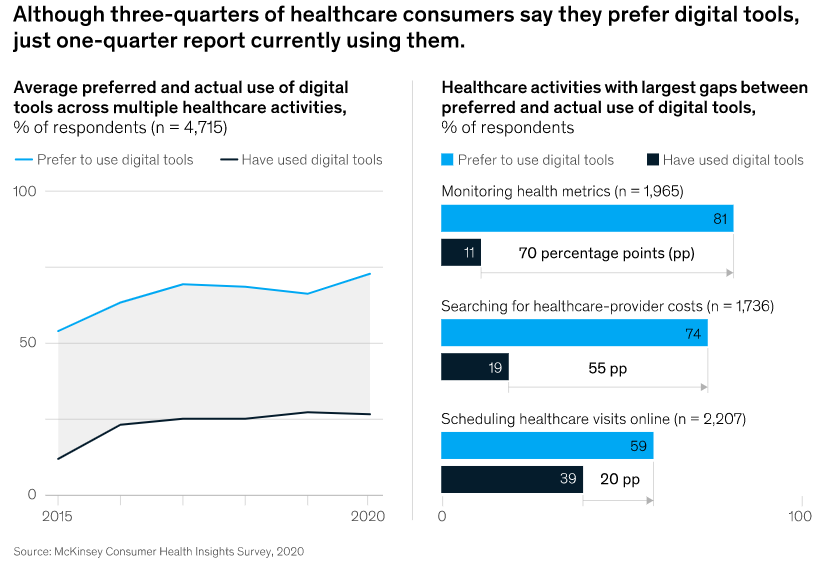

Earlier in the week McKinsey reported that "While a majority of healthcare consumers say they prefer digital tools across all healthcare-related activities, the percentage of consumers who actually use digital tools remains low. Some of the largest opportunities to increase digital use include monitoring health metrics, searching for healthcare-provider costs, and scheduling appointments online."

What is missing here in the picture is also the availability. When people prefer using digital tools, but they are not available, then of course there is a gap. And the lack of availability might be due to a mismatch of their need or condition and what's available or even more likely due to limitations of their health insurance.

Of course, there are people who are willing to pay extra out of their own pocket and get digital health service quickly, even if they would be otherwise covered with a longer wait of in-person healthcare service. But for accelerating the mainstream use of digital health tools, insurers need to join these efforts as well.

It's like digital banking. Many legacy banks feel like there's little need for innovation and it's still OK to require people to visit their physical branch offices for frequent procedures. On the other hand, as a customer of Wise, N26 and Revolut I have never been to any of their offices and everything I needed, starting with account creation, has been fully digital. And despite DBS claims in Singapore to have voted as "best online banking experience in Singapore", most likely the ones in that poll had never used Wise, N26 and Revolut.

While developing Nursebeam I've had many discussions with both insurers and travellers, to bring the availability of our digital travel health services to all those who get sick abroad. And we have seen the willingness of people to pay extra even when their insurance does not cover, to get care quickly and without the bureaucratic hassles. Still, for the mainstream of customers, insurance coverage is relevant.

I believe that when enabling people to use digital health tools and services, so that their insurance is covering it (like they would the in-person visits), we'd also see the current gap between talk and action also closing.

Hopefully, legacy health insurers and healthcare providers realise that they are like banks... and if they don't innovate quick enough, healthtechs will. They are the ones offering the action, beyond the legacy talks.

Member discussion